ck0001592900-20230930

4979/30/20230001592900falseN-1A4.99xbrli:pureiso4217:USD0001592900ck0001592900:C000237974Memberck0001592900:S000077497Member2024-06-212024-06-2100015929002024-06-212024-06-210001592900ck0001592900:S000077497Member2024-06-212024-06-210001592900rr:RiskLoseMoneyMemberck0001592900:S000077497Member2024-06-212024-06-210001592900ck0001592900:S000077497Memberrr:RiskNotInsuredDepositoryInstitutionMember2024-06-212024-06-210001592900ck0001592900:S000077497Memberck0001592900:OptionsRiskMember2024-06-212024-06-210001592900ck0001592900:OptionsRiskSellingOrWritingOptionsMemberck0001592900:S000077497Member2024-06-212024-06-210001592900ck0001592900:S000077497Memberck0001592900:OptionsRiskBuyingOrPurchasingOptionsRiskMember2024-06-212024-06-210001592900ck0001592900:OptionsRiskBoxSpreadRiskMemberck0001592900:S000077497Member2024-06-212024-06-210001592900ck0001592900:S000077497Memberck0001592900:OptionsRiskFLEXOptionsRiskMember2024-06-212024-06-210001592900ck0001592900:S000077497Memberck0001592900:CounterpartyRiskMember2024-06-212024-06-210001592900ck0001592900:LowShortTermInterestRatesRiskMemberck0001592900:S000077497Member2024-06-212024-06-210001592900ck0001592900:S000077497Memberck0001592900:InvestmentRiskMember2024-06-212024-06-210001592900ck0001592900:S000077497Memberck0001592900:ManagementRiskMember2024-06-212024-06-210001592900ck0001592900:S000077497Memberck0001592900:MarketRiskMember2024-06-212024-06-210001592900ck0001592900:S000077497Memberck0001592900:TaxRiskMember2024-06-212024-06-210001592900ck0001592900:ValuationRiskMemberck0001592900:S000077497Member2024-06-212024-06-210001592900ck0001592900:S000077497Memberck0001592900:ETFRisksMember2024-06-212024-06-210001592900ck0001592900:ETFRiskLimitedNumberOfAuthorizedParticipantsMarketMakersAndLiquidityProvidersMemberck0001592900:S000077497Member2024-06-212024-06-210001592900ck0001592900:S000077497Memberck0001592900:ETFRiskPremiumDiscountRiskMember2024-06-212024-06-210001592900ck0001592900:ETFRiskCostOfTradingRiskMemberck0001592900:S000077497Member2024-06-212024-06-210001592900ck0001592900:ETFRiskTradingRiskMemberck0001592900:S000077497Member2024-06-212024-06-210001592900ck0001592900:S000077497Memberck0001592900:CashTransactionsRiskMember2024-06-212024-06-210001592900ck0001592900:S000077497Memberck0001592900:LargeShareholderRiskMember2024-06-212024-06-210001592900ck0001592900:S000077497Memberck0001592900:CashAndCashEquivalentsRiskMember2024-06-212024-06-210001592900ck0001592900:FrequentTradingRiskMemberck0001592900:S000077497Member2024-06-212024-06-210001592900ck0001592900:S000077497Memberck0001592900:LimitedOperatingHistoryRiskMember2024-06-212024-06-210001592900ck0001592900:GeopoliticalNaturalDisasterRisksMemberck0001592900:S000077497Member2024-06-212024-06-210001592900ck0001592900:S000077497Memberck0001592900:Solactive13MonthUSTBillIndexreflectsnodeductionforfeesorexpensesIndexMember2024-06-212024-06-210001592900ck0001592900:C000237974Memberrr:AfterTaxesOnDistributionsMemberck0001592900:S000077497Member2024-06-212024-06-210001592900ck0001592900:C000237974Memberck0001592900:S000077497Memberrr:AfterTaxesOnDistributionsAndSalesMember2024-06-212024-06-21

sAlpha

Architect 1-3 Month Box ETF

Ticker

Symbol: BOXX

(a

series of EA Series Trust)

Prospectus

February 28,

2024

(as

supplemented June 24,

2024)

Listed

on Cboe BZX Exchange, Inc.

These

securities have not been approved or disapproved by the Securities and Exchange

Commission nor has the Securities and Exchange Commission passed upon the

accuracy or adequacy of this Prospectus. Any representation to the contrary is a

criminal offense.

Table

of Contents

ALPHA

ARCHITECT 1-3 MONTH BOX ETF

INVESTMENT

OBJECTIVE

The

Alpha

Architect 1-3 Month Box ETF (the “Fund”) seeks to provide

investment results that, before fees and expenses, equals or exceeds the price

and yield performance of an investment that tracks the 1-3 month sector of the

United States Treasury Bill market.

FEES AND

EXPENSES

This

table describes the fees and expenses that you may pay if you buy, hold, and

sell shares of the Fund (“Shares”). You

may also pay brokerage commissions on the purchase and sale of Shares, which are

not reflected in the table or example.

ANNUAL FUND

OPERATING EXPENSES (EXPENSES THAT YOU PAY EACH YEAR AS A PERCENTAGE OF THE VALUE

OF YOUR INVESTMENT)

|

|

|

|

|

| |

| Management

Fee |

0.3949 |

% |

| Distribution

and/or Service (12b-1) Fees |

0.00 |

% |

|

Other

Expenses |

0.00 |

% |

| Total

Annual Fund Operating Expenses |

0.3949 |

% |

|

Fees

Waived and/or Reimbursed1 |

(0.20) |

% |

| Total

Annual Fund Operating Expenses After Waiving and/or Reimbursing

Expenses |

0.1949 |

% |

1The

Adviser has contractually agreed to waive receipt of its management fees and/or

assume expenses of the Fund so that the total annual operating expenses of the

Fund (excluding payments under the Fund’s Rule 12b-1 distribution and service

plan (if any), acquired fund fees and expenses, brokerage expenses, taxes

(including tax-related services), interest (including borrowing costs),

litigation expense (including class action-related services) and other

non-routine or extraordinary expenses) do not exceed 0.1949% of the Fund’s

average daily net assets. This agreement will remain in place until at least

February 28, 2025. The agreement may be

terminated only by the Board of Trustees.

EXAMPLE

The following example is intended to help you compare the cost of

investing in the Fund with the cost of investing in other funds. The example

assumes that you invest $10,000 for the time periods indicated and then redeem

all of your Shares at the end of those periods. The example reflects the Fund’s

contractual expense limitation agreement only for the term of the contractual

expense limitation agreement. The example also assumes that the Fund provides a

return of 5% a year and that operating expenses remain the same. You may also

pay brokerage commissions on the purchase and sale of Shares, which are not

reflected in the example. Although your actual

costs may be higher or lower, based on these assumptions your costs would

be:

|

|

|

|

|

|

|

|

|

|

|

| |

| One

Year: |

Three

Years: |

Five

Years: |

Ten

Years: |

| $20 |

$107 |

$201 |

$479 |

PORTFOLIO

TURNOVER

The

Fund may pay transaction costs, including commissions when it buys and sells

securities (or “turns over” its portfolio). A higher portfolio turnover rate may

indicate higher transaction costs and may result in higher taxes when Shares are

held in a taxable account. These costs, which are not reflected in annual fund

operating expenses or in the example, affect the Fund’s performance. For the

fiscal period ended October 31, 2023, the Fund’s portfolio turnover rate was

0%

of the average value of its portfolio. This rate excludes the value of portfolio

securities whose maturities or expiration dates at the time of acquisition were

one year or less.

PRINCIPAL INVESTMENT

STRATEGIES

Alpha

Architect 1-3 Month Box ETF (the “Fund”) is an actively managed exchange-traded

fund (“ETF”) whose investment objective is to provide investment results that,

before fees and expenses, equal or exceed the price and yield performance of an

investment that tracks the 1-3 month sector of the United States Treasury Bill

market. To do so, the principal investment strategy of the Fund will be to

utilize a series of long and short exchange-listed options combinations called a

box spread (“Box Spread”). In order to accomplish its investment goals, the Fund

may utilize either standard exchange-listed options or FLexible EXchange®

Options (“FLEX Options”) or a combination of both.

In

general, an option contract is an agreement between a buyer and seller that

gives the purchaser of the option the right to buy or sell a particular asset at

a specified future date at an agreed upon price, commonly known as the “strike

price.” In the case of a “call option”, the purchaser has the right to buy the

particular asset and the seller of a “call option” has the obligation to deliver

the particular asset at the strike price. In the case of a “put option”, the

purchaser has the right to sell the particular asset and the seller of a “put

option” has the obligation to deliver the particular asset at the strike

price.

By

way of background, a Box Spread is the combination of a synthetic long position

coupled with an offsetting synthetic short position through a combination of

options contracts on an equity security or an equity index at the same

expiration date. The synthetic long consists of buying a call option and selling

a put option on the same security or index where the call option and put option

share the same strike and expiration date (a “Synthetic Long”). When purchasing

a Box Spread, the Synthetic Long will have a strike price that is less than the

strike price for the Synthetic Short. The difference between the strike prices

of the Synthetic Long and the Synthetic Short will determine the expiration

value (or value at maturity) of the Box Spread. The synthetic short consists of

buying a put option and selling a call option on the same security or index with

the same expiration date as the synthetic long but using a different strike

price (a “Synthetic Short”). When purchasing a Box Spread, the Synthetic Long

will have a strike price that is less than the strike price for the Synthetic

Short. The difference between the strike prices of the Synthetic Long and the

Synthetic Short will determine the expiration value (or value at maturity) of

the Box Spread. An important feature of the Box Spread construction process is

the elimination of risk tied to underlying market movements associated with the

underlying option’s security or equity index. As displayed in the diagram below,

the Box Spread return stays constant no matter how low or how high the

underlying option’s security or equity index price moves. Once the Box Spread is

initiated, its return from the initiation date of such Box Spread through its

expiration date will generally not change. The Fund anticipates buying, holding,

and/or selling multiple Box Spreads, and consequently, the Fund’s anticipated

return from Box Spreads will reflect all of its investment activity, as well as

changes in market prices and expected interest rates, among other factors, and

will vary over time.

Buying

(or selling) a Box Spread is similar to buying (or selling) a zero-coupon bond.

A zero-coupon bond does not pay periodic coupons, but the bond trades

at a discount to its face value. The maturity value of a zero-coupon

bond is comparable to the difference in the strike prices of the Box Spread. The

maturity date of a zero-coupon bond is comparable to the expiration date of the

options comprising the Box Spread. When constructing a Box Spread, the strike

price of the Synthetic Long will be at a lower strike price than the strike

price of the Synthetic Short. When buying or selling a Box Spread, the buyer or

seller generally expects the price of the Box Spread to be less than the

difference in the strike prices of the Box Spread. A buyer or seller of a Box

Spread will earn a profit or loss equal to the difference between the beginning

price (price paid to buy or received if sold) and the ending price (expiration

value or closing trade price). If the Fund holds the Box Spread until

expiration, then its profit or loss will be determined by the difference between

the price it paid to buy the Box Spread (or received in the case of selling the

Box Spread) and the value of the Box Spread upon expiration.

As

an example, a typical Box Spread could include the simultaneous purchase of a

call option and sale of a put option (i.e. Synthetic Long) with a strike of

$1,000 on the S&P 500 Index (“SPX”) together with the sale of a call option

and purchase of a put option (i.e. Synthetic Short) with a strike of $2,000 on

the SPX where all four of these options share the same expiration date. The

expiration or maturity value would be the difference in the strikes or $1,000 in

this case. The expected profit earned would equal the difference between the

price paid for this Box Spread and its expiration value of $1,000 minus any

transaction costs associated with the options trades. The effective yield on

each Box Spread is determined by annualizing the profit over the price paid. The

Fund will only purchase Box Spreads where the purchase price (after considering

all costs to the Fund for entering such trade) is less than the expiration

value.

Arin

Risk Advisors, LLC (“Arin”) may invest the Fund’s assets in a series of Box

Spreads with various expiration dates. The quantity and expiration dates of the

Box Spreads held by the Fund will be based on several factors, including the

Fund’s asset size, the effective yield for various Box Spread expiration dates

available in the marketplace, and Arin’s view of future interest rates. Based

upon historical examples of Box Spreads actually traded in the marketplace, Arin

expects that there will be market participants willing to sell Box Spreads to

the Fund in sufficient quantities to satisfy the objective of the

Fund.

Under normal

market conditions, the Fund generally invests substantially all, but at least

80%, of its total assets in a series of Box Spreads such that the weighted

average maturity of the Box Spreads based upon expiration dates is less than 90

days. The Fund may sell Box Spreads with a longer or shorter

period to expiration in an effort to gain

exposure

to the forward rate implied by the execution of longer and shorter dated Box

Spreads. The Fund expects to trade some or all of the Box Spreads prior to their

respective expiration dates, if Arin believes it is advantageous for the Fund to

do so. Upon expiration or sale of any Box Spread, Arin may seek to purchase

additional Box Spreads at an effective yield and expiration date that offers

favorable risk and reward characteristics under current market conditions. The

Fund may also invest in cash, cash equivalents, money market funds or treasury

bills. The Fund’s strategy is expected to result in high portfolio turnover. The

return that the Fund expects to earn from Box Spreads will fluctuate but remain

consistent with the market rate for similar short-term interest rate sensitive

securities as indicated by the Federal Funds Futures market.

When

purchasing or selling a Box Spread, the Fund will primarily use European-style

options. European style options may not be terminated or assigned in advance of

the option’s expiration date and may only be exercised on their expiration date.

This ensures that none of the synthetic positions created using the Box Spread

will be forcibly closed prior to the Box Spread’s maturity. The Fund expects to

use options on broad-based diversified assets such as the SPDR® S&P 500® ETF

Trust for substantially all of the Fund’s holdings. The Fund may purchase or

sell Box Spreads using exchange-listed option contracts on an ETF other than the

SPDR® S&P 500® ETF Trust or on an index or individual equity security when

Arin has determined that doing so would provide the Fund with better risk and

return or tax characteristics. The Fund may also utilize an exchange-listed

options strategy using long shares of an individual equity security or ETF (in

place of the Synthetic Long) together with a Synthetic Short created by

purchasing a put option and selling a call option on that equity security or ETF

with the same strike and expiration date. This individual equity security or ETF

strategy will generally be purchased when such purchase is in the best interest

of the Fund because it offers more favorable price or tax characteristics. The

Fund’s collateral will typically be utilized to fully pay for the Box Spreads or

other similar strategies as described above.

The

Fund may engage in active and frequent trading of portfolio securities to

achieve its investment objective. In order to achieve its objective, the Fund

will typically purchase a new Box Spread at the time (or shortly thereafter) any

existing Box Spread expires or is sold or when Arin believes purchasing a new

Box Spread would offer a favorable investment opportunity. The Fund may also

sell or “roll” any Box Spread at any time. When rolling a Box Spread, the Fund

enters into a trade where it simultaneously closes on each component of an

existing Box Spread while opening a new Box Spread position. The Fund may also

sell Box Spreads that utilize the same or a different reference assets, strike

prices, and expiration dates as Box Spreads owned by the Fund. When selling or

rolling a Box Spread, the Fund may incur additional transaction costs than if it

waited until such Box Spread expired.

Exchange-traded options on certain indexes, such as the SPX, are

currently taxed under section 1256 of the Internal Revenue Code of 1986 (the

“Code”). Pursuant to section 1256 of the Code, profit and loss on transactions

in non-equity options, including SPX options, are subject to taxation at a rate

equal to 60% long-term and 40% short-term capital gain or loss regardless of the

Fund’s holding period. Based on the advice of its accountants, the Fund expects

that distributions related to the Fund’s SPX positions, if any, will be

characterized by the Fund as capital gains with these preferential terms. The

Fund expects that distributions, if any, related to the Fund’s positions that do

not qualify for the preferential treatment under section 1256 are expected to be

characterized by the Fund as either short-term capital gain or ordinary

income.

PRINCIPAL

RISKS

An

investment in the Fund involves risk, including those described below.

There

is no assurance that the Fund will achieve its investment objective.

An

investor may lose money by investing in the Fund. An investment in

the Fund is not a bank deposit and is not insured or guaranteed by the FDIC or

any government agency. More complete risk descriptions are set

forth below under the heading “Additional

Information About the Fund’s Risks”.

Options

Risk.

•Selling

or Writing Options.

Writing option contracts can result in losses that exceed the seller’s initial

investment and may lead to additional turnover and higher tax liability. The

risk involved in writing a call option is that there could be an increase in the

market value of the underlying or reference asset. An underlying or reference

asset may be an index, equity security, or ETF. If this occurs, the call option

could be exercised and the underlying asset would then be sold at a lower price

than its current market value. In the case of cash settled call options such as

SPX options, the call seller would be required to purchase the call option at a

price that is higher than the original sales price for such call option.

Similarly, while writing

call

options can reduce the risk of owning the underlying asset, such a strategy

limits the opportunity to profit from an increase in the market value of the

underlying asset in exchange for up-front cash at the time of selling the call

option. The risk involved in writing a put option is that there could be a

decrease in the market value of the underlying asset. If this occurs, the put

option could be exercised and the underlying asset would then be sold at a

higher price than its current market value. In the case of cash settled put

options, the put seller would be required to purchase the put option at a price

that is higher than the original sales price for such put

option.

•Buying

or Purchasing Options Risk.

If a call or put option is not sold when it has remaining value and if the

market price of the underlying asset, in the case of a call option, remains less

than or equal to the exercise price, or, in the case of a put option, remains

equal to or greater than the exercise price, the buyer will lose its entire

investment in the call or put option. Since many factors influence the value of

an option, including the price of the underlying asset, the exercise price, the

time to expiration, the interest rate, and the dividend rate of the underlying

asset, the buyer’s success in implementing an option buying strategy may depend

on an ability to predict movements in the prices of individual assets,

fluctuations in markets, and movements in interest rates. There is no assurance

that a liquid market will exist when the buyer seeks to close out any option

position. When an option is purchased to hedge against price movements in an

underlying asset, the price of the option may move more or less than the price

of the underlying asset.

•Box

Spread Risk.

A Box Spread is the combination of a Synthetic Long position coupled with an

offsetting Synthetic Short position through a combination of options contracts

on an underlying or reference asset such as index, equity security or ETF with

the same expiration date. A Box Spread typically consists of four option

positions two of which represent the Synthetic Long and two representing the

Synthetic Short. If one or more of these individual option positions are

modified or closed separately prior to the option contract’s expiration, then

the Box Spread may no longer effectively eliminate risk tied to underlying

asset’s movement. Furthermore, the Box Spread’s value is derived in the market

and is in part, based on the time until the options comprising the Box Spread

expire and the prevailing market interest rates. If the Fund sells a Box Spread

prior to its expiration, then the Fund may incur a loss. The Fund’s ability to

profit from Box Spreads is dependent on the availability and willingness of

other market participants to sell Box Spreads to the Fund at competitive

prices.

•FLEX

Options Risk.

FLEX

Options are exchange-traded options contracts with uniquely customizable terms

like exercise price, style, and expiration date. Due to their customization and

potentially unique terms, FLEX Options may be less liquid than other securities,

such as standard exchange listed options. In less liquid markets for the FLEX

Options, the Fund may have difficulty closing out certain FLEX Options positions

at desired times and prices. The value of FLEX Options will be affected by,

among others, changes in the underlying share or equity index price, changes in

actual and implied interest rates, changes in the actual and implied volatility

of the underlying shares or equity index and the remaining time to until the

FLEX Options expire. The value of the FLEX Options will be determined based upon

market quotations or using other recognized pricing methods. During periods of

reduced market liquidity or in the absence of readily available market

quotations for the holdings of the Fund, the ability of the Fund to value the

FLEX Options becomes more difficult and the judgment of Arin (employing the fair

value procedures adopted by the Board of Trustees of the Trust) may play a

greater role in the valuation of the Fund’s holdings due to reduced availability

of reliable objective pricing

data.

Counterparty

Risk. Counterparty

risk is the risk that a counterparty to a financial instrument held by the Fund

or by a special purpose or structured vehicle invested in by the Fund may become

insolvent or otherwise fail to perform its obligations, and the Fund may obtain

no or limited recovery of its investment, and any recovery may be significantly

delayed. Exchange listed options, including FLEX Options, are issued and

guaranteed for settlement by the Options Clearing Corporation (“OCC”). The

Fund’s investments are at risk that the OCC will be unable or unwilling to

perform its obligations under the option contract terms. In the unlikely event

that the OCC becomes insolvent or is otherwise unable to meet its settlement

obligations, the Fund could suffer significant

losses.

Low

Short-Term Interest Rates Risk.

During market conditions in which short-term interest rates are at low levels,

the Fund’s yield can be very low, and the Fund may have a negative yield (i.e.,

it may lose money on an operating basis). During these conditions, it is

possible that the Fund will generate an insufficient amount of income

to

pay its expenses. In addition, it is possible that during these conditions the

Fund may experience difficulties purchasing and/or selling securities with

respect to scheduled rebalances, and may, as a result, maintain a portion of its

assets in cash, on which it may earn little, if any,

income.

Investment

Risk. When

you sell your Shares of the Fund, they could be worth less than what you paid

for them. The Fund could lose money due to short-term interest rate market

movements and over longer periods during continued interest rate market

movements. Therefore, you may lose money by investing in the

Fund.

Management

Risk.

The Fund is actively managed and may not meet its investment objective based on

Arin’s success or failure to implement investment strategies for the Fund. In

addition, there is the risk that the investment process, techniques and analyses

used by Arin will not produce the desired investment results and the Fund may

lose value as a result.

Market

Risk.

The Fund’s investments are subject to changes in general economic conditions,

general market fluctuations and the risks inherent in investment in interest

rate sensitive markets. Interest rate markets can be volatile and prices of

investments can change substantially due to various factors including, but not

limited to, economic growth or recession, the investment’s average time to

maturity, changes in interest rates, changes in the actual or perceived

creditworthiness of issuers, and general market liquidity. The Fund is subject

to the risk that geopolitical events will disrupt securities markets and

adversely affect global economies and markets. Local, regional or global events

such as war, acts of terrorism, the spread of infectious illness or other public

health issues, or other events could have a significant impact on the Fund and

its investments.

Tax

Risk.

The Fund may enter into various transactions for which there is a lack of clear

guidance under the Code, which may affect the taxation of the Fund or its

distributions to shareholders. In particular, the use of certain derivatives may

cause the Fund to realize higher amounts of ordinary income or short-term

capital gain, to suspend or eliminate holding periods of positions, and/or to

defer realized losses, potentially increasing the amount of taxable

distributions, and of ordinary income distributions in particular. In addition,

certain derivatives are subject to mark-to-market or straddle provisions of the

Code. If such provisions are applicable, there could be an increase (or

decrease) in the amount of taxable distributions paid by the Fund. The Fund

intends to qualify as a regulated investment company (“RIC”) under the Code,

which requires the Fund to distribute a certain portion of its income and gains

each tax year, among other requirements. Similar to other ETFs and pursuant to

the Code, when the Fund disposes of appreciated property by distributing such

appreciated property in-kind pursuant to redemption requests, the Fund does not

recognize any built-in gain in such appreciated property. If the Internal

Revenue Service (“IRS”) disagrees with the Fund’s position as to the

applicability of this non-recognition rule to the Fund’s disposition of

derivatives, the Fund may not have distributed sufficient income or gains to

qualify as a RIC. If, in any year, the Fund fails to qualify as a RIC, the Fund

itself generally would be subject to U.S. federal income and potentially excise

taxation and distributions received by its shareholders generally would be

subject to further U.S. federal income taxation. Failure to comply with the

requirements for qualification as a RIC would have significant negative economic

and tax consequences to Fund shareholders. Additionally, section 1258 of the

Code requires that gain be recharacterized as ordinary income if it is derived

from any transaction in which substantially all of the expected return is

attributable to the time value of the investment in such transaction and which

falls into certain categories defined in the Code (a “conversion transaction”).

If any of the Fund’s transactions are deemed to be conversion transactions,

gains recognized, if any, from such transactions would be treated as ordinary

income, which could result in the Fund being under-distributed with the same

consequences as described above. It may be asserted that the Fund itself has

engaged in conversion transactions, the mere holding of Shares by a Fund

shareholder is a conversion transaction, or

both.

Valuation

Risk.

Some portfolio holdings, potentially a large portion of the Fund’s investment

portfolio, may be valued on the basis of factors other than market quotations.

This may occur more often in times of market turmoil or reduced liquidity. There

are multiple methods that can be used to value a portfolio holding when market

quotations are not readily available. The value established for any portfolio

holding at a point in time might differ from what would be produced using a

different methodology or if it had been priced using market

quotations.

Portfolio

holdings that are valued using techniques other than market quotations,

including “fair valued” securities, may be subject to greater fluctuation in

their valuations from one day to the next than if market quotations were used.

In addition, there is no assurance that the Fund could sell or close out a

portfolio position for the value

established

for it at any time, and it is possible that the Fund would incur a loss because

a portfolio position is sold or closed out at a discount to the valuation

established by the Fund at that

time.

ETF

Risks.

•Authorized

Participants, Market Makers and Liquidity Providers Concentration Risk.

The

Fund has a limited number of financial institutions that may act as Authorized

Participants (“APs”). In particular, the Fund will have a limited pool of APs

that are able to transact in standard exchange-listed options as well as FLEX

Options, therefore the pool of competitive markets for the Fund will be small.

This can result in increased costs to the Fund. In addition, there may be a

limited number of market makers and/or liquidity providers in the marketplace.

To the extent either of the following events occur, Shares may trade at a

material discount to NAV and possibly face delisting: (i) APs exit the business

or otherwise become unable to process creation and/or redemption orders and no

other APs step forward to perform these services, or (ii) market makers and/or

liquidity providers exit the business or significantly reduce their business

activities and no other entities step forward to perform their

functions.

•Premium-Discount

Risk.

The Shares may trade above or below their net asset value (“NAV”). The

market prices of Shares will generally fluctuate in accordance with changes in

NAV as well as the relative supply of, and demand for, Shares on Cboe BZX

Exchange, Inc. (the “Exchange”) or other securities exchanges. The trading price

of Shares may deviate significantly from NAV during periods of market volatility

or limited trading activity in Shares. In addition, you may incur the cost of

the “spread,” that is, any difference between the bid price and the ask price of

the Shares.

•Cost

of Trading Risk.

Investors

buying or selling Shares in the secondary market will pay brokerage commissions

or other charges imposed by brokers as determined by that broker. Brokerage

commissions are often a fixed amount and may be a significant proportional cost

for investors seeking to buy or sell relatively small amounts of

Shares.

•Trading

Risk.

Although

the Shares are listed on the Exchange, there can be no assurance that an active

or liquid trading market for them will develop or be maintained. In addition,

trading in Shares on the Exchange may be halted. In stressed market conditions,

the liquidity of Shares may begin to mirror the liquidity of its underlying

portfolio holdings, which can be less liquid than Shares, potentially causing

the market price of Shares to deviate from its NAV. The spread varies over time

for Shares of the Fund based on the Fund’s trading volume and market liquidity

and is generally lower if the Fund has high trading volume and market liquidity,

and higher if the Fund has little trading volume and market liquidity (which is

often the case for funds that are newly launched or small in

size).

Cash

Transactions Risk. Unlike most other ETFs, the Fund expects to effect a substantial

portion of its creations for cash, rather than in-kind securities. Cash creation

transactions may result in certain brokerage, tax, execution, price movement and

other costs and expenses related to the execution of trades resulting from such

transactions, and these costs and expenses are typically reimbursed to the Fund

by the AP placing the order(s). To the extent that the maximum additional charge

for creation transactions is insufficient to cover these costs and expenses, the

Fund’s performance could be negatively impacted. The use of cash creations may

also cause the Fund’s shares to trade in the market at greater bid-ask spreads

or greater premiums or discounts to the Fund’s NAV. Further, an investment in

the Fund may be less tax-efficient than an investment in an ETF that effects its

redemptions only in-kind. ETFs are able to make in-kind redemptions and avoid

being taxed on gains on the distributed portfolio securities at the fund level.

A Fund that effects redemptions for cash may be required to sell portfolio

securities to obtain the cash needed to distribute redemption proceeds. Any

recognized gain on these sales by the Fund will generally cause the Fund to

recognize a gain it might not otherwise have recognized, or to recognize such

gain sooner than would otherwise be required if it were to distribute portfolio

securities only in-kind. The Fund intends to distribute these gains to

shareholders to avoid being taxed on this gain at the fund level. As a practical

matter, only institutions and large investors, such as market makers or other

large broker dealers, create or redeem shares directly through the Fund. Most

investors will buy and sell shares of the Fund on an exchange through a

broker-dealer.

Large

Shareholder Risk. Certain

large shareholders, including other funds advised by the Fund’s investment

adviser or sub-advisers, may from time to time own a substantial amount of the

Fund’s Shares. Any such investment may be held for a limited period of time.

There can be no assurance that any large shareholder will not redeem its

investment.

Dispositions of a large number of Shares by such shareholders, which may occur

rapidly or unexpectedly, may adversely affect the Fund’s liquidity and net

assets to the extent such transactions are executed directly with the Fund in

the form of redemptions through an AP, rather than executed in the secondary

market. To the extent effected in cash, these redemptions may also force the

Fund to sell portfolio securities when it might not otherwise do so, which may

negatively impact the Fund’s NAV and increase the Fund’s brokerage costs. Such

cash redemptions may also accelerate the realization of taxable income to

shareholders. Similarly, large Fund share purchases through an AP may adversely

affect the performance of the Fund to the extent that the Fund is delayed in

investing new cash or otherwise maintains a larger cash position than it

ordinarily would. If these large shareholders transact in Shares on the

secondary market, such transactions may account for a large percentage of the

Fund’s trading volume and may, therefore, have a material upward or downward

effect on the market price of the

Shares.

Cash

and Cash Equivalents Risk.

Holding cash or cash equivalents rather than securities or other instruments in

which the Fund primarily invests, even strategically, may cause the Fund to risk

losing opportunities to earn increased returns, and may cause the Fund to

experience potentially lower returns than the Fund’s benchmark or other funds

that remain fully invested.

Frequent

Trading Risk.

The Fund may engage in active and frequent trading of portfolio securities to

achieve its investment objective. This frequent trading of portfolio securities

may increase the amount of commissions that the Fund pays when it buys and sells

such portfolio securities, which may detract from the Fund’s performance.

Derivative instruments and instruments with a maturity of one year or less at

the time of acquisition are excluded from the calculation of the Fund’s

portfolio turnover rate, which leads to the 0% portfolio turnover rate reported

herein.

Limited

Operating History Risk.

The Fund is a recently organized investment company with a limited operating

history. As a result, prospective investors have a limited track record or

history on which to base their investment decision.

Geopolitical/Natural

Disaster Risks. The Fund’s investments are subject to geopolitical and natural

disaster risks, such as war, terrorism, trade disputes, political or economic

dysfunction within some nations, public health crises and related geopolitical

events, as well as environmental disasters, epidemics and/or pandemics, which

may add to instability in world economies and volatility in markets. The impact

may be short-term or may last for extended periods.

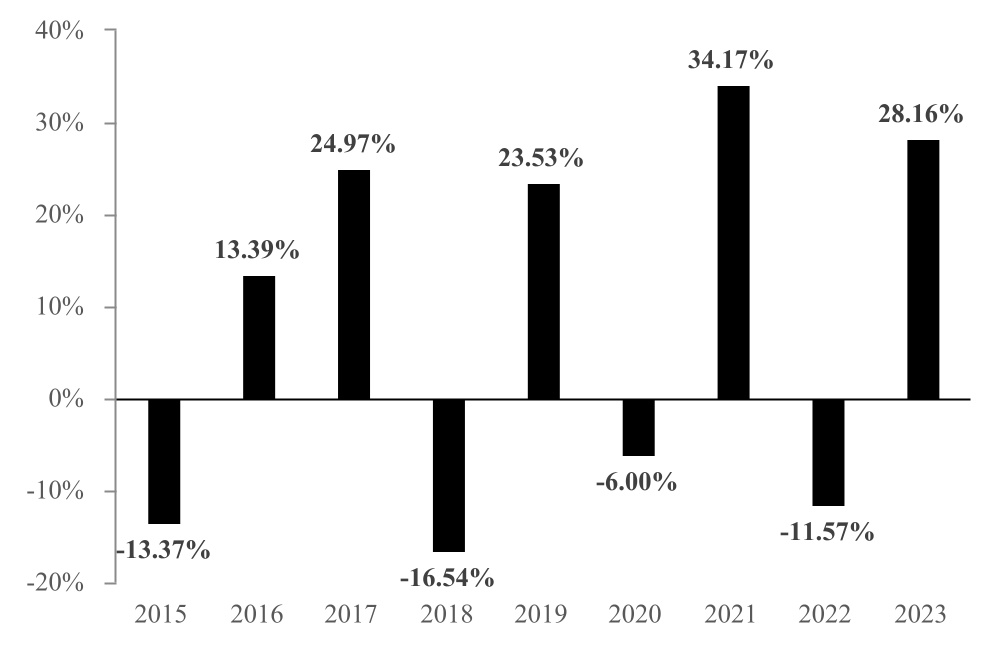

PERFORMANCE

The

following information provides some indication of the risks of investing in the

Fund. The bar chart shows the Fund’s performance for calendar years ended

December 31. The table shows how the Fund’s average annual returns for one-year

and since inception periods compare with those of a broad measure of market

performance. The Fund’s past performance, before and after taxes, is not

necessarily an indication of how the Fund will perform in the future.

Performance information is also available on the Fund’s website at

www.alphaarchitect.com/funds or by calling the

Fund at (215) 882-9983.

Calendar Year Total Return as

of December 31

During

the period of time shown in the bar chart, the Fund’s highest

return for a calendar quarter was 1.37% (quarter ended

December 31,

2023) and the Fund’s lowest

return for a calendar quarter was 1.11% (quarter ended June 30,

2023).

|

|

|

|

|

|

|

|

| |

|

Average

Annual Total Returns

(for

periods ended December 31, 2023) |

1

Year |

Since

Inception

(12/27/22) |

|

Return Before

Taxes |

4.99% |

4.97% |

|

Return After

Taxes on Distributions |

4.99% |

4.97% |

|

Return After

Taxes on Distributions and Sale of Shares |

2.95% |

3.79% |

|

Solactive

1-3 Month US T-Bill Index (reflects

no deduction for fees or expenses)1 |

5.12% |

5.12% |

1Index

assumes withholding taxes on dividends.

After-tax returns are calculated using the highest historical

individual U.S. federal marginal income tax rates during the period covered by

the table and do not reflect the impact of state and local

taxes. Actual

after-tax returns depend on your tax situation and may differ from those shown

and are not relevant if you hold your shares through a tax- deferred

arrangement, such as a 401(k) plan or an individual retirement account

(“IRA”).

The

Solactive 1-3 month US T-Bill Index is a rules-based, market value weighted

index engineered for the short-term T-Bill market denominated in USD. The index

is comprised of USD denominated T-Bills with a time to maturity of 1 to 3

months.

INVESTMENT

ADVISER & INVESTMENT SUB-ADVISERS

|

|

|

|

|

| |

|

Investment

Adviser: |

Empowered

Funds, LLC dba EA Advisers (“Adviser”) |

| Investment

Sub-Advisers: |

Arin

Risk Advisors, LLC (“Arin”)

Alpha

Architect, LLC (“Alpha Architect”) |

PORTFOLIO

MANAGERS

The

Fund’s portfolio is managed on a day-to-day basis by Lawrence Lempert, Joseph

DeSipio, and Ryan Bailey. Messrs. Lempert, DeSipio and Bailey have managed the

Fund since its inception in 2022.

PURCHASE

AND SALE OF FUND SHARES

The

Fund issues and redeems Shares on a continuous basis only in large blocks of

Shares, typically 10,000 Shares, called “Creation Units,” and only APs

(typically, broker-dealers) may purchase or redeem Creation Units. Creation

Units are primarily issued in cash and redeemed ‘in-kind’ for securities and/or

in cash. Individual Shares may only be purchased and sold in secondary market

transactions through brokers. Once created, individual Shares generally trade in

the secondary market at market prices that change throughout the day. Market

prices of Shares may be greater or less than their NAV. Except

when aggregated in Creation Units, the Fund’s shares are not redeemable

securities.

TAX

INFORMATION

The

Fund’s distributions generally are taxable to you as ordinary income, capital

gain, or some combination of both, unless your investment is in an IRA or other

tax-advantaged account. However, subsequent withdrawals from such a

tax-advantaged account may be subject to U.S. federal income tax. In the event

that a shareholder purchases Shares shortly before a distribution by the Fund,

the entire distribution may be taxable to the shareholder even though a portion

of the distribution effectively represents a return of the purchase price. You

should consult your own tax advisor about your specific tax

situation.

PURCHASES

THROUGH BROKER-DEALERS AND OTHER FINANCIAL INTERMEDIARIES

If

you purchase Shares through a broker-dealer or other financial intermediary, the

Fund and its related companies may pay the intermediary for the sale of Shares

and related services. These payments may create a conflict of interest by

influencing the broker-dealer or other intermediary and your salesperson to

recommend Shares over another investment. Ask your salesperson or visit your

financial intermediary’s website for more information.

ADDITIONAL

INFORMATION ABOUT THE FUND

How

is the Fund Different from a Mutual Fund?

Redeemability.

Mutual

fund shares may be bought from, and redeemed with, the issuing fund for cash at

NAV typically calculated once at the end of the business day. Shares of the

Fund, by contrast, cannot be purchased from or redeemed with the Fund except by

or through APs (typically, broker-dealers), and then principally for cash for

purchases and an in-kind basket of securities (and a limited cash amount) for

redemptions. In addition, the Fund issues and redeems Shares on a continuous

basis only in large blocks of Shares, typically 10,000 Shares, called “Creation

Units.”

Exchange

Listing. Unlike

mutual fund shares, Shares of the Fund will be listed for trading on the

Exchange. Investors can purchase and sell Shares on the secondary market through

a broker. Investors purchasing Shares in the secondary market through a

brokerage account or with the assistance of a broker may be subject to brokerage

commissions and charges. Secondary-market transactions do not occur at NAV, but

at market prices that change throughout the day, based on the supply of, and

demand for, Shares and on changes in the prices of the Fund’s portfolio

holdings. The market price of Shares may differ from the NAV of the Fund. The

difference between the market price of Shares and the NAV of the Fund is called

a premium when the market price is above the reported NAV and called a discount

when the market price is below the reported NAV, and the difference is expected

to be small most of the time, though it may be significant, especially in times

of extreme market volatility.

Tax

Treatment. The

Fund and the Shares have been designed to be tax-efficient where possible. To

the extent redemptions from the Fund are paid in cash, the Fund may realize

capital gains or losses, including in some cases short-term capital gains, upon

the sale of portfolio securities to generate the cash to satisfy the redemption.

In addition, tax treatment of options may negate certain tax efficiencies

typically associated with an ETF. As a result, an investment in the Fund may be

less tax-efficient than an investment in an ETF that effects its redemptions

only in-kind.

Transparency.

The

Fund’s portfolio holdings are disclosed on its website daily after the close of

trading on the Exchange and prior to the opening of trading on the Exchange the

following day. A description of the Fund’s policies and procedures with respect

to the disclosure of the Fund’s portfolio holdings is available in the Fund’s

Statement of Additional Information (“SAI”).

Premium/Discount

Information. Information

about the premiums and discounts at which the Fund’s Shares have traded will be

available at www.alphaarchitect.com/funds.

ADDITIONAL

INFORMATION ABOUT THE FUND’S INVESTMENT OBJECTIVE AND STRATEGIES

The

Fund’s investment objective is a non-fundamental investment policy and may be

changed without a vote of shareholders with prior written notice to

shareholders.

The

Fund is an actively managed ETF whose investment objective is to provide

investment results that, before fees and expenses, equal or exceed the price and

yield performance of an investment that tracks the 1-3 month sector of the

United States Treasury Bill. To do so, the principal investment strategy of the

Fund will be to utilize a series of long and short exchange-listed options

combinations called a box spread (“Box Spread”). In order to accomplish its

investment goals, the Fund may utilize either standard exchange-listed options

or FLEX Options or a combination of both.

In

general, an option contract is an agreement between a buyer and seller that

gives the purchaser of the option the right to buy or sell a particular asset at

a specified future date at an agreed upon price, commonly known as the “strike

price.” In the case of a “call option”, the purchaser has the right to buy the

particular asset and the seller of a “call option” has the obligation to deliver

the particular asset at the strike price. In the case of a “put option”, the

purchaser has the right to sell the particular asset and the seller of a “put

option” has the obligation to deliver the particular asset at the strike

price.

By

way of backgroun, a Box Spread is the combination of a synthetic long position

coupled with an offsetting synthetic short position through a combination of

options contracts on an equity security or an equity index at the same

expiration date. The synthetic long consists of buying a call option and selling

a put option on the same security or index where the call option and put option

share the same strike and expiration date (a “Synthetic Long”).

When

purchasing a Box Spread, the Synthetic Long will have a strike price that is

less than the strike price for the Synthetic Short. The difference between the

strike prices of the Synthetic Long and the Synthetic Short will determine the

expiration value (or value at maturity) of the Box Spread. The synthetic short

consists of buying a put option and selling a call option on the same security

or index with the same expiration date as the synthetic long but using a

different strike price (a “Synthetic Short”). When purchasing a Box Spread, the

Synthetic Long will have a strike price that is less than the strike price for

the Synthetic Short. The difference between the strike prices of the Synthetic

Long and the Synthetic Short will determine the expiration value (or value at

maturity) of the Box Spread. An important feature of the Box Spread construction

process is the elimination of risk tied to underlying market movements

associated with the underlying option’s security or equity index. The Box Spread

return stays constant no matter how low or how high the underlying option’s

security or equity index price moves. Once the Box Spread is initiated, its

return from the initiation date of such Box Spread through its expiration date

will generally not change. The Fund anticipates buying, holding, and/or selling

multiple Box Spreads, and consequently, the Fund’s anticipated return from Box

Spreads will reflect all of its investment activity, as well as changes in

market prices and expected interest rates, among other factors, and will vary

over time.

Buying

(or selling) a Box Spread is similar to buying (or selling) a zero-coupon bond.

A zero-coupon bond does not pay periodic coupons, but the bond trades

at a discount to its face value. The maturity value of a zero-coupon

bond is comparable to the difference in the strike prices of the Box Spread. The

maturity date of a zero-coupon bond is comparable to the expiration date of the

options comprising the Box Spread. When constructing a Box Spread, the strike

price of the Synthetic Long will be at a lower strike price than the strike

price of the Synthetic Short. When buying or selling a Box Spread, the buyer or

seller generally expects the price of the Box Spread to be less than the

difference in the strike prices of the Box Spread. A buyer or seller of a Box

Spread will earn a profit or loss equal to the difference between the beginning

price (price paid to buy or received if sold) and the ending price (expiration

value or closing trade price). If the Fund holds the Box Spread until

expiration, then its profit or loss will be determined by the difference between

the price it paid to buy the Box Spread (or received in the case of selling the

Box Spread) and the value of the Box Spread upon expiration.

As

an example, a typical Box Spread could include the simultaneous purchase of a

call option and sale of a put option (i.e. Synthetic Long) with a strike of

$1,000 on the S&P 500 Index (“SPX”) together with the sale of a call option

and purchase of a put option (i.e. Synthetic Short) with a strike of $2,000 on

the SPX where all four of these options share the same expiration date. The

expiration or maturity value would be the difference in the strikes or $1,000 in

this case. The expected profit earned would equal the difference between the

price paid for this Box Spread and its expiration value of $1,000 minus any

transaction costs associated with the options trades. The effective yield on

each Box Spread is determined by annualizing the profit over the price paid. The

Fund will only purchase Box Spreads where the purchase price (after considering

all costs to the Fund for entering such trade) is less than the expiration

value.

Arin

may invest the Fund’s assets in a series of Box Spreads with various expiration

dates. The quantity and expiration dates of the Box Spreads held by the Fund

will be based on several factors, including the Fund’s asset size, the effective

yield for various Box Spread expiration dates available in the marketplace, and

Arin’s view of future interest rates. Based upon historical examples of Box

Spreads actually traded in the marketplace, Arin expects that there will be

market participants willing to sell Box Spreads to the Fund in sufficient

quantities to satisfy the objective of the Fund.

Under

normal market conditions, the Fund generally invests substantially all, but at

least 80%, of its total assets in a series of Box Spreads such that the weighted

average maturity of the Box Spreads based upon expiration dates is less than 90

days. The Fund may sell Box Spreads with a longer or shorter period to

expiration in an effort to gain exposure to the forward rate implied by the

execution of longer and shorter dated Box Spreads. The Fund expects to trade

some or all of the Box Spreads prior to their respective expiration dates, if

Arin believes it is advantageous for the Fund to do so.Upon expiration or sale

of any Box Spread, Arin will seek to purchase additional Box Spreads at an

effective yield and expiration date that offers favorable risk and reward

characteristics under current market conditions. The Fund may also invest in

cash, cash equivalents, money market funds or treasury bills. The Fund’s

strategy is expected to result in high portfolio turnover. The return that the

Fund expects to earn from Box Spreads will fluctuate but remain consistent with

the market rate for similar short-term interest rate sensitive securities as

indicated by the Federal Funds Futures market.

When

purchasing or selling a Box Spread, the Fund will primarily use European-style

options. European style options may not be terminated or assigned in advance of

the option’s expiration date and may only be exercised on their expiration date.

This ensures that none of the synthetic positions created using the Box Spread

will be forcibly closed cancelled prior to the Box Spread’s maturity. The Fund

expects to use options on the SPDR® S&P 500® ETF Trust for substantially all

of the Fund’s holdings. The Fund may purchase or sell Box Spreads using

exchange-listed option contracts on an ETF other than the SPDR® S&P 500® ETF

Trust or on an index or individual equity security when Arin has determined that

doing so would provide the Fund with better risk and return or tax

characteristics. The Fund may also utilize an exchange-listed options strategy

using long shares of an individual equity security or ETF (in place of the

Synthetic Long) together with a Synthetic Short created by purchasing a put

option and selling a call option on that equity security or ETF with the same

strike and expiration date. This individual equity security or ETF strategy will

generally be purchased when such purchase is in the best interest of the Fund

because it offers more favorable price or tax characteristics. The Fund’s

collateral will typically be utilized to fully pay for the Box Spreads or other

similar strategies as described above.

The

Fund may engage in active and frequent trading of portfolio securities to

achieve its investment objective. In order to achieve its objective, the Fund

will typically purchase a new Box Spread at the time (or shortly thereafter) any

existing Box Spread expires or is sold or when Arin believes purchasing a new

Box Spread would offer a favorable investment opportunity. The Fund may also

sell or “roll” any Box Spread at any time. When rolling a Box Spread, the Fund

enters into a trade where it simultaneously closes on each component of an

existing Box Spread while opening a new Box Spread position. The Fund may also

sell Box Spreads that utilize the same or a different reference assets, strike

prices, and expiration dates as Box Spreads owned by the Fund. When selling or

rolling a Box Spread, the Fund may incur additional transaction costs than if it

waited until such Box Spread expired.

Exchange-traded

options on certain indexes, such as the SPX, are currently taxed under section

1256 of the Code. Pursuant to section 1256 of the Code, profit and loss on

transactions in non-equity options, including SPX options, are subject to

taxation at a rate equal to 60% long-term and 40% short-term capital gain or

loss regardless of the Fund’s holding period. Based on the advice of its

accountants, the Fund expects that distributions related to the Fund’s SPX

positions, if any, will be characterized by the Fund as capital gains with these

preferential terms.

Alpha

Architect works closely with Arin as it relates to providing strategic

investment advice to the Fund.

ADDITIONAL

INFORMATION ABOUT THE FUND’S RISKS

The

following information is in addition to, and should be read along with, the

description of the Fund’s principal investment risks in the sections titled

“Fund Summary—Principal Investment Risks” above.

Cash

and Cash Equivalents Risk.

Holding cash or cash equivalents rather than securities or other instruments in

which the Fund primarily invests, even strategically, may cause the Fund to risk

losing opportunities to earn increased returns, and may cause the Fund to

experience potentially lower returns than the Fund’s benchmark or other funds

that remain fully invested.

Cash

Transactions Risk.

Unlike most other ETFs, the Fund expects to effect a substantial portion of its

creations for cash, rather than in-kind securities. Cash creation transactions

may result in certain brokerage, tax, execution, price movement and other costs

and expenses related to the execution of trades resulting from such

transactions, and these costs and expenses are typically reimbursed to the Fund

by the AP placing the order(s). To the extent that the maximum additional charge

for creation transactions is insufficient to cover these costs and expenses, the

Fund’s performance could be negatively impacted. The use of cash creations may

also cause the Fund’s shares to trade in the market at greater bid-ask spreads

or greater premiums or discounts to the Fund’s NAV. Further, an investment in

the Fund may be less tax-efficient than an investment in an ETF that effects its

redemptions only in-kind. ETFs are able to make in-kind redemptions and avoid

being taxed on gains on the distributed portfolio securities at the fund level.

A Fund that effects redemptions for cash may be required to sell portfolio

securities to obtain the cash needed to distribute redemption proceeds. Any

recognized gain on these sales by the Fund will generally cause the Fund to

recognize a gain it might not otherwise have recognized, or to recognize such

gain sooner than would otherwise be required if it were to distribute portfolio

securities only in-kind. The Fund intends to distribute these gains to

shareholders to avoid being taxed on this gain at the fund level. This strategy

may cause shareholders to be subject to tax on gains they would not otherwise be

subject to, or at an earlier date than if they had made an investment in a

different ETF. As a practical matter, only institutions and large investors,

such as market makers or other large

broker

dealers, create or redeem shares directly through the Fund. Most investors will

buy and sell shares of the Fund on an exchange through a broker-dealer.

Counterparty

Risk. Counterparty

risk is the risk that a counterparty to a financial instrument held by the Fund

may become insolvent or otherwise fail to perform its obligations, and the Fund

may obtain no or limited recovery of its investment, and any recovery may be

significantly delayed. Exchange listed options, including FLEX Options, are

issued and guaranteed for settlement by the Options Clearing Corporation

(“OCC”). The Fund bears the risk that the OCC will be unable or unwilling to

perform its obligations under the options contracts. In the unlikely event that

the OCC becomes insolvent or is otherwise unable to meet its settlement

obligations, the Fund could suffer significant losses. Additionally, FLEX

Options may be illiquid, and in such cases, the Fund may have difficulty closing

out certain FLEX Options positions at desired times and prices. Also, since the

Fund is not a member of the OCC (a “clearing member”), and only clearing members

can participate directly in the OCC, the Fund will hold options contracts

through commingled omnibus accounts at clearing members. As a result, Fund

assets deposited with a clearing member as margin for options contracts may, in

certain circumstances, be used to satisfy losses of other clients of the Fund’s

clearing member. Although clearing members guarantee performance of their

clients’ obligations to the OCC, there is a risk that Fund assets might not be

fully protected in the event of the clearing member’s bankruptcy.

Geopolitical/Natural

Disaster Risks.

The Fund’s investments are subject to geopolitical and natural disaster risks,

such as war, terrorism, trade disputes, political or economic dysfunction within

some nations, public health crises and related geopolitical events, as well as

environmental disasters, epidemics and/or pandemics, which may add to

instability in world economies and volatility in markets. The impact may be

short-term or may last for extended periods.

ETF

Risks.

•Authorized

Participants, Market Makers and Liquidity Providers Concentration Risk.

The

Fund has a limited number of financial institutions that may act as Authorized

Participants (“APs”). In particular, the Fund will have a limited pool of APs

that are able to transact in standard exchange-listed options as well as FLEX

Options, therefore the pool of competitive markets for the Fund will be small.

This can result in increased costs to the Fund. In addition, there may be a

limited number of market makers and/or liquidity providers in the marketplace.

To the extent either of the following events occur, Shares may trade at a

material discount to NAV and possibly face delisting: (i) APs exit the business

or otherwise become unable to process creation and/or redemption orders and no

other APs step forward to perform these services, or (ii) market makers and/or

liquidity providers exit the business or significantly reduce their business

activities and no other entities step forward to perform their

functions.

•Premium-Discount

Risk.

The

Shares may trade above or below their net asset value (“NAV”). The market prices

of Shares will generally fluctuate in accordance with changes in NAV as well as

the relative supply of, and demand for, Shares on the Exchange or other

securities exchanges. The trading price of Shares may deviate significantly from

NAV during periods of market volatility or limited trading activity in Shares.

In addition, you may incur the cost of the “spread,” that is, any difference

between the bid price and the ask price of the Shares.

•Cost

of Trading Risk.

Investors

buying or selling Shares in the secondary market will pay brokerage commissions

or other charges imposed by brokers as determined by that broker. Brokerage

commissions are often a fixed amount and may be a significant proportional cost

for investors seeking to buy or sell relatively small amounts of Shares. In

addition, secondary market investors will also incur the cost of the difference

between the price that an investor is willing to pay for Shares (the “bid”

price) and the price at which an investor is willing to sell Shares (the “ask”

price). This difference in bid and ask prices is often referred to as the

“spread” or “bid/ask spread.” The bid/ask spread varies over time for Shares

based on trading volume and market liquidity, and is generally lower if Shares

have more trading volume and market liquidity and higher if Shares have little

trading volume and market liquidity. Further, increased market volatility may

cause increased bid/ask spreads.

•Trading

Risk.

Although

the Shares are listed on the Exchange, there can be no assurance that an active

or liquid trading market for them will develop or be maintained. In addition,

trading in Shares on the

Exchange

may be halted due to market conditions or for reasons that, in the view of the

Exchange, make trading in Shares inadvisable. When markets are stressed, Shares

could suffer erratic or unpredictable trading activity, extraordinary volatility

or wide bid/ask spreads, which could cause some market makers and APs to reduce

their market activity or “step away” from making a market in ETF shares. This

could cause the Fund’s market price to deviate, materially, from the NAV, and

reduce the effectiveness of the ETF arbitrage process. Further, trading in

Shares on the Exchange is subject to trading halts caused by extraordinary

market volatility pursuant to the “circuit breaker” rules, which temporarily

halt trading on the Exchange when a decline in the S&P 500 Index during a

single day reaches certain thresholds (e.g., 7%, 13% and 20%). There can be no

assurance that the requirements of the Exchange necessary to maintain the

listing of the Fund will continue to be met or will remain unchanged. In

stressed market conditions, the liquidity of Shares may begin to mirror the

liquidity of the Fund’s underlying portfolio holdings, which can be

significantly less liquid than Shares, and this could lead to differences

between the market price of the Shares and the underlying value of those

Shares.

Frequent

Trading Risk.

The Fund may engage in active and frequent trading of portfolio securities to

achieve its investment objective. In order to achieve its objective, the Fund

will purchase a new Box Spread at the time (or shortly thereafter) any existing

Box Spread expires. The Fund may also “roll” any Box Spread at any time. When

rolling a Box Spread, the Fund enters into a trade where it simultaneously

closes on each component of an existing Box Spread while opening a new Box

Spread position. In rolling a Box Spread, the Fund will incur additional

transaction costs than if it waited until such Box Spread expired. This frequent

trading of portfolio securities may increase the amount of commissions that the

Fund pays when it buys and sells such portfolio securities, which may detract

from the Fund’s performance.

Derivative

instruments and instruments with a maturity of one year or less at the time of

acquisition are excluded from the calculation of the Fund’s portfolio turnover

rate, which leads to the 0% portfolio turnover rate reported

herein.

Investment

Risk. When

you sell your Shares of the Fund, they could be worth less than what you paid

for them. During a general downturn in the securities markets, multiple asset

classes may be negatively affected. Therefore, you may lose money by investing

in the Fund.

Large

Shareholder Risk.

Certain large shareholders, including other funds advised by the Fund’s

investment adviser or sub-advisers, may from time to time own a substantial

amount of the Fund’s Shares. Any such investment may be held for a limited

period of time. There can be no assurance that any large shareholder will not

redeem its investment. Dispositions of a large number of Shares by such

shareholders, which may occur rapidly or unexpectedly, may adversely affect the

Fund’s liquidity and net assets to the extent such transactions are executed

directly with the Fund in the form of redemptions through an authorized

participant, rather than executed in the secondary market. To the extent

effected in cash, these redemptions may also force the Fund to sell portfolio

securities when it might not otherwise do so, which may negatively impact the

Fund’s NAV and increase the Fund’s brokerage costs. Such cash redemptions may

also accelerate the realization of taxable income to shareholders. Similarly,

large Fund share purchases through an authorized participant may adversely

affect the performance of the Fund to the extent that the Fund is delayed in

investing new cash or otherwise maintains a larger cash position than it

ordinarily would. If these large shareholders transact in Shares on the

secondary market, such transactions may account for a large percentage of the

Fund’s trading volume and may, therefore, have a material upward or downward

effect on the market price of the Shares.

Limited

Operating History Risk.

The Fund is a recently organized investment company with a limited operating

history. As a result, prospective investors have a limited track record or

history on which to base their investment decision.

Low

Short-Term Interest Rates Risk.

During market conditions in which short-term interest rates are at low levels,

the Fund’s yield can be very low, and the Fund may have a negative yield (i.e.,

it may lose money on an operating basis). During these conditions, it is

possible that the Fund will generate an insufficient amount of income to pay its

expenses. In addition, it is possible that during these conditions the Fund may

experience difficulties purchasing and/or selling securities with respect to

scheduled rebalances, and may, as a result, maintain a portion of its assets in

cash, on which it may earn little, if any, income.

Management

Risk. The

Fund is actively managed and may not meet its investment objective based on

Arin’s success or failure to implement investment strategies for the Fund.

Arin’s evaluations and assumptions regarding

investments

may not successfully achieve the Fund’s investment objective given actual market

trends. In addition, there is the risk that Arin’s investment process,

techniques and analyses will not produce the desired investment results and the

Fund may lose value as a result.

Market

Risk.

The Fund’s investments are subject to changes in general economic conditions,

general market fluctuations and the risks inherent in investment in securities

markets. Investment markets can be volatile and prices of investments can change

substantially due to various factors including, but not limited to, economic

growth or recession, changes in interest rates, changes in the actual or

perceived creditworthiness of issuers, and general market liquidity. The Fund is

subject to the risk that geopolitical events will disrupt securities markets and

adversely affect global economies and markets. Local, regional or global events

such as war, acts of terrorism, the spread of infectious illness or other public

health issues, or other events could have a significant impact on the Fund and

its investments.

Options

Risk.

•Selling

or Writing Options Risks.

Writing

option contracts can result in losses that exceed the seller’s initial

investment and may lead to additional turnover and higher tax liability. The

risk involved in writing a call option is that there could be an increase in the

market value of the underlying or reference asset. An underlying or reference

asset may be an index, equity security, or ETF. If this occurs, the call option

could be exercised and the underlying asset would then be sold at a lower price

than its current market value. In the case of cash settled call options such as

SPX options, the call seller would be required to purchase the call option at a

price that is higher than the original sales price for such call option.

Similarly, while writing call options can reduce the risk of owning the

underlying asset, such a strategy limits the opportunity to profit from an

increase in the market value of the underlying asset in exchange for up-front

cash at the time of selling the call option. The risk involved in writing a put

option is that there could be a decrease in the market value of the underlying

asset. If this occurs, the put option could be exercised and the underlying

asset would then be sold at a higher price than its current market value. In the

case of cash settled put options, the put seller would be required to purchase

the put option at a price that is higher than the original sales price for such

put option.

•Buying

or Purchasing Options Risk.

If a call or put option is not sold when it has remaining value and if the

market price of the underlying asset, in the case of a call option, remains less

than or equal to the exercise price, or, in the case of a put, remains equal to

or greater than the exercise price, the buyer will lose its entire investment in

the call or put option. Since many factors influence the value of an option,

including the price of the underlying asset, the exercise price, the time to

expiration, the interest rate, and the dividend rate of the underlying asset,

the buyer’s success in implementing the an option buying strategy may depend on

an ability to predict movements in the prices of individual assets, fluctuations

in markets, and movements in interest rates. There is no assurance that a liquid

market will exist when the buyer seeks to close out an option position. When an

option is purchase to hedge against price movements in an underlying asset, the

price of the option may move more or less than the price of the underlying

asset.

•Box

Spread Risk.

A Box Spread is the combination of a Synthetic Long position coupled with an

offsetting Synthetic Short position through a combination of options contracts

on an underlying or referenced asset such as index, equity security or ETF with

the same expiration date. A Box Spread typically consists of four option

positions two of which represent the Synthetic Long and two representing the

Synthetic Short. If one or more of these individual option positions are

modified or closed separately prior to the option contract’s expiration, then

the Box Spread may no longer effectively eliminate risk tied to underlying

asset’s movement. Furthermore, the Box Spread’s value is derived in the market

and is in part, based on the time until the options comprising the Box Spread

expire and the prevailing market interest rates. If the Fund sells a Box Spread

prior to its expiration, then the Fund may incur a loss. The Fund’s ability to

profit from Box Spreads is dependent on the availability and willingness of

other market participants to sell Box Spreads to the Fund at competitive

prices.

•FLEX

Options Risk.

FLEX